From CBRE

Germany’s real estate investment market stages significant year-end recovery

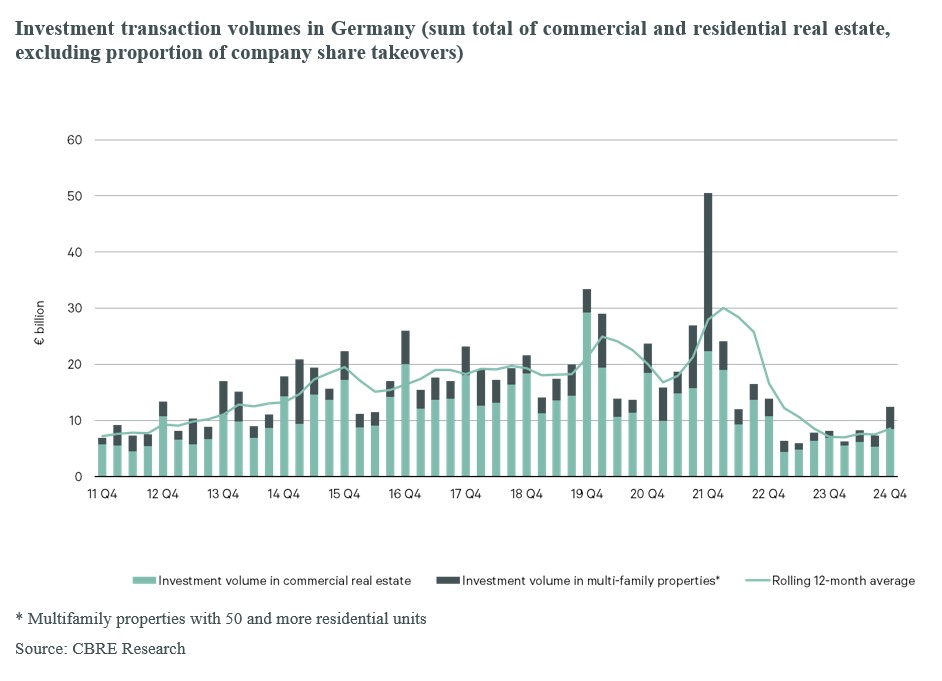

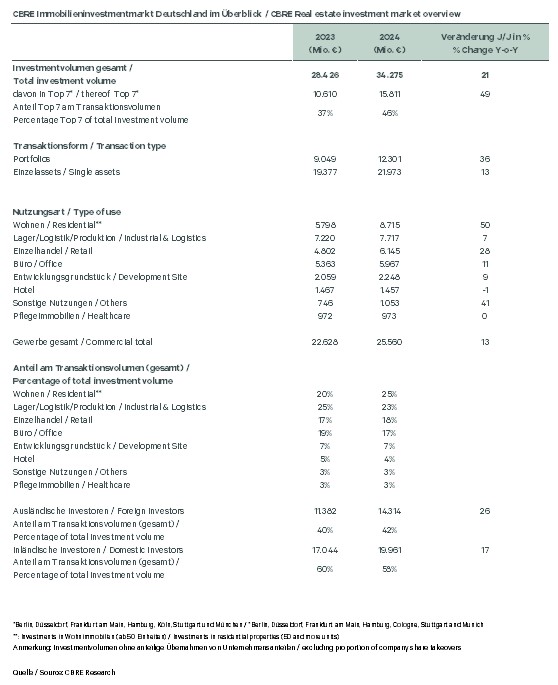

The German real estate investment market recorded a transaction volume of €34.3 billion in 2024. Compared with 2023, this reflects growth of 21 percent. At €12.4 billion, the final quarter of 2024 exceeded that of 2023 by 52 percent – and by 69 percent quarter on quarter. Multifamily housing (upward of 50 units) that accounted for a share of around one quarter of the overall volume held its place as the strongest asset class, followed closely by logistics properties (23 percent). Retail properties took a share of 18 percent and were marginally ahead of office (17 percent), along with hotel and healthcare properties that settled around the year-earlier level (four and three percent respectively). Moreover, 2024 saw significantly more large-scale deals again. At €17 billion, approximately half the overall volume was attributable to transactions above the €100 million mark (in 2023, this figure posted only €11 billion). This volume was attributable to 72 large-scale transactions – in 2023, there were only 45. These are the conclusions drawn in a current analysis prepared by the global commercial real estate services company CBRE.

“We have a very dynamic year-end rally behind us, which marks the start of a new cycle in the investment market. Investor confidence is growing thanks to an attractive interest rate environment and consequently greater predictability with business plans,”

says Kai Mende, CBRE Germany’s CEO.

“Strong impetus is currently emanating from monetary policies. While, from an investor standpoint, interest rates have become more attractive again, most investors have adjusted to a higher-for-longer environment. Conservative plans are therefore coinciding with more positive framework conditions, which is a good starting point for the real estate investment market,” explains Dr. Jan Linsin, Head of Research at CBRE Germany.

Start of moderate yield compression

The process of repricing that began in 2021 in the core segment across all asset classes has meanwhile come to an end, and the signs point to an onset of a moderate yield compression. This onset was observed in the segment of high street properties (expressed as an average of the Top 7 cities, down 0.2 percentage points to 4.6 percent compared with the third quarter of 2024), partly in the office segment (down 0.2 percentage points in Berlin and Munich to 4.8 and 4.6 percent respectively) and with logistics properties (Berlin’s market area aside, down 0.1 percentage points to 4.4 percent). The prime yields of operator real estate such as hotels and healthcare properties have nevertheless remained stable for the time being. “At the current point in time, many real estate segments offer favorable entry prices, particularly in combination with anticipating ongoing mild yield compression in the first half of the year. However, all asset classes are displaying polarization as, in the case of non-prime properties, the market will continue to see capital values decline over the course of 2025 as well,” says Mende in anticipation.

A comparison with real estate yields shows the following: the yield of 10-year Bunds settled at 2.43 percent at the end of 2024 (up 0.24 percentage points above the figure posted at the start of 2024), the five-year Euro swap came in at 2.2 percent (down 0.21 percentage points) and the 10-year Euro swap at 2.32 percent (down 0.15 percentage points). “Investing in real estate is becoming increasingly attractive in the current interest rate environment. This is also borne out by our discussions with institutional investors who remain convinced of the German market and are prepared to pay somewhat higher prices again in the bidding procedure, which in turn has prompted the recent market recovery. Yield compression in the prime segment is likely to continue in the majority of asset classes as the year progresses,” Linsin states.

Top 7 markets more important

The proportion of the Top 7 locations in the overall volume has increased significantly again. In 2024, this share stood at 46 percent, which is nine percentage points more than in 2023. At just under €6 billion, half of which in residential investment, Berlin continued in first place, with 37 percent more invested than in the previous year. The transaction volume increased even more significantly in Munich that took second place – up 57 percent to a good €3 billion. At €2.3 billion, Hamburg took third place, clocking up 41 percent more than in 2023, followed by Frankfurt am Main with just under €1.6 billion (up 104 percent). More than one billion was invested in the two Rhineland cities of Düsseldorf (€1.4 billion, up 155 percent) and Cologne (€1.1 billion, up 44 percent). Stuttgart’s real estate investment market was alone in sustaining a decline of 28 percent to around €400 million.

Asset and fund managers made gains

The strongest net buyers proved to be asset and fund managers that invested almost €2.9 billion more than they sold. They were followed by corporates with a positive balance of €1.4 billion. Open-ended real estate and special funds also produced a positive balance (€284 million). In this case, however, special funds opted more for buying, as opposed to open-ended mutual funds that were keener on selling owing to the current environment. At the same time, international investors earmarked significantly more funds for investment again compared with 2023. In absolute terms, their investment volume rose by 26 percent, lifting their share by two percentage points to 42 percent. The strongest international investor group consisted of asset and fund managers, along with listed property companies/REITs. Players from other European countries outside Germany were particularly active on the German real estate investment market.

Outlook for 2025

“There are signs that the positive momentum from the fourth quarter of 2024 is set to continue in 2025. A transaction volume of up to €40 billion on Germany’s real estate investment market is possible for the full year,” Mende says. “Active asset management will be decisive for the success of real estate investments. Those who know the ins and outs of the real estate business can hope for a good year.”

“The year 2025 will be one of investment opportunities although the economy, especially in Germany, is facing huge challenges, both structural and economic. Be that as it may, Germany’s parliamentary elections in February also give rise to big hopes for rebooting the country’s economy and realigning the ‘Made in Germany’ business model,” Linsin explains.

*In addition to the transaction volume, minority stakes of €278 million were registered. Financing transactions are not included.